Financial statements are essentially a small business owner’s entrepreneurial blueprint.

Not only do they allow business owners to keep track of spending, but they also serve as a company’s credentials, should any potential investors show interest.

By keeping an ongoing, organized record of financial statements, small business owners can spend less time worrying about daunting administrative tasks like budgeting and put more energy into the day-to-day operations of the company.

Understanding your financial statements

Whether you work with an accountant or do your own bookkeeping, it’s important to have a solid grasp of your finances—and that means understanding all the components of your financial statements. Financial statements are broken down into three main statements: the income statement, the balance sheet, and the cash flow statement.

Together, these three components help to give small business owners a more clear idea of their company’s financial expenditures.

Balance sheets

Balance sheets are perhaps the simplest part of any financial statement. Short and sweet, they resemble an invoice, and include a lengthy tally of business costs with the total sum at the bottom of the page.

Balance sheets outline the business’s existing assets, as well as any outstanding liabilities or debts owed, existing investments, and any stockholder equities at a given point in time.

They allow the business owner, as well as any potential investors, to review the company’s overall financial operations and examine any financial limitations that would prohibit or hinder a partnership.

The number of balance sheets a business creates per year will ultimately depend on its overall financial position. Larger companies, or those with substantial revenue streams, may benefit from putting together a balance sheet every day, or on a weekly basis so that they may better track profit or loss.

Small business owners who might not yet have built up substantial financial collateral may find that making a balance sheet on a monthly basis will suffice. The decision is ultimately up to the company and how they wish to track their financial spending.

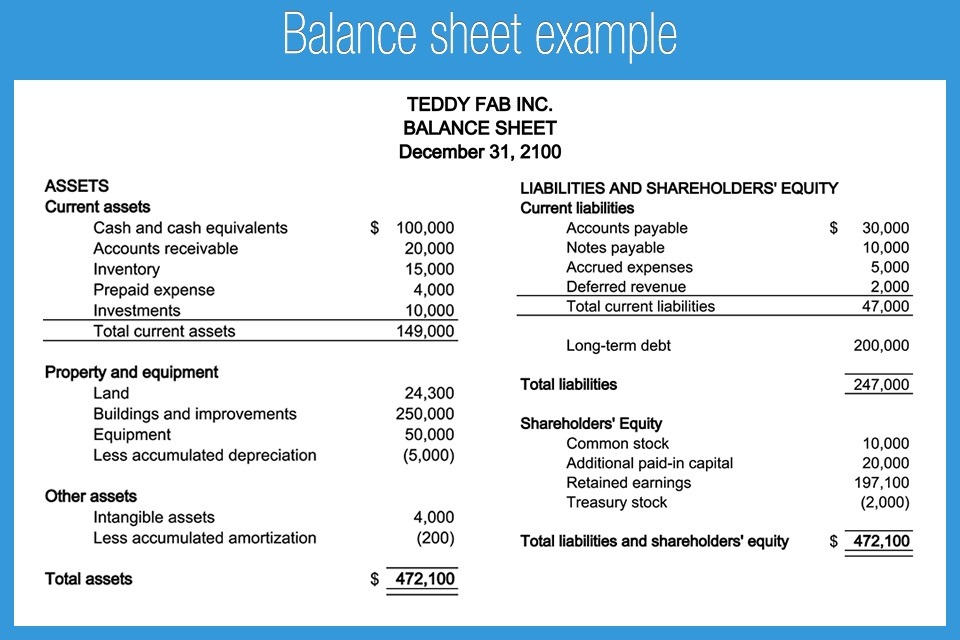

Here’s an example of what a typical balance sheet looks like:

From the example image above, the following can be determined from the balance sheet:

- The company has $149,000 in current assets, including cash and cash equivalents, accounts receivable, inventory, prepaid expenses, and investments.

- All property and equipment owned by the company account for $329,300.

- The company is liable for a total of $47,000, which includes its accounts payable, notes payable, accrued expenses, and deferred revenue.

- The company also still has $200,000 in outstanding, long-term debt, which could refer to a line of credit, a bank loan, or bonds that have reached maturity before one year. This raises the total cost of liabilities to $247,000.

- Shareholders’ equity accounts for $472,100, and includes common stock, additional paid-in capital, retained earnings (leftover net income from the business, after it pays out its dividends to shareholders), and treasury stock (outstanding stock repurchased from stockholders).

As outlined, the balance sheet is broken down further to dissect assets, liabilities, and shareholder’s equity.

The following three elements can be found on any balance sheet:

Assets

Assets are defined as anything and everything that the company has full ownership of. In this particular case, this includes cash and cash equivalents, accounts receivable, all current inventory, prepaid expenses, and additional investments.

Finances aside, assets can also represent a company’s land and any buildings or offices connected to the company, equipment (including office supplies), and any accumulated depreciation accounts (an asset account with an existing credit balance).

Liabilities

Liabilities are outstanding debts owed by the business. In the photo example above, the largest liability for the business in question is their accounts payable.

This could mean that the company has several outstanding invoices that have not yet been paid to their suppliers or has yet to pay out employee salaries.

Additional liabilities can include mortgages, credit card debts, and any ongoing expenses that are directly connected to the business, like property taxes, utility bills, and additional operating costs that exist to keep the company afloat.

Equity

Small business owners can realize the equity of their company once the liabilities are subtracted from the assets.

The most commonly recognized form of equity on a financial statement is the revenue that the business has earned to date.

In the example above, the business has mixed equity of common stock (purchased shares that can be sold off) and additional paid-in capital (monies that investors pay).

Equity always refers to what is called the business’s “book value,” which means the total amount that the business has in funds at a given moment in time.

If a small business owner were to turn around and sell the company, the existing equity does not represent the true market value.

For example, just because a homeowner spends $100,000 on renovations prior to selling does not mean that they will collect an additional $100,000 as a result of those investments when the time comes to put the house on the market.

With a simple mathematical equation, understanding equity is easy:

Equity = Assets – Liabilities.

Income statements

The income statement is where small business owners can see how their company actually profited during an accounting period (monthly, quarterly, yearly).

Balance sheets, on the other hand, only tell a business owner how financials were doing at a given point in time (individual days or weeks, for example).

Income statements are sometimes called profit and loss statements, and they allow business owners to track their earnings (revenue) and their spending (business expenses).

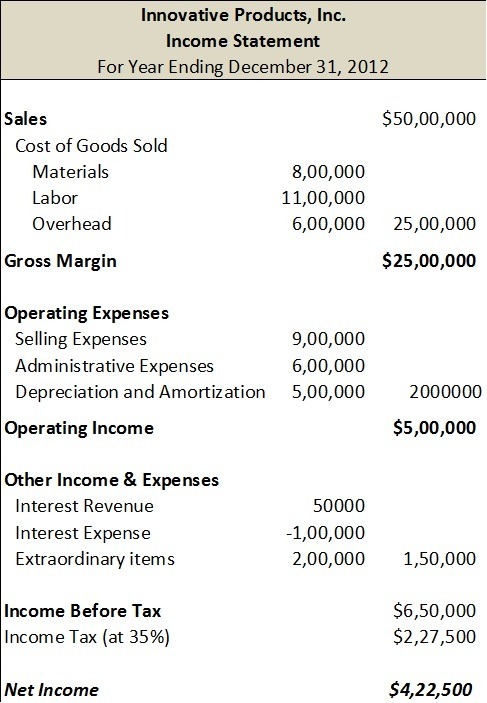

The below image is an example of a typical income statement:

Income statements, like balance sheets, are divided into several parts, including sales, gross profits, operating expenses, operating income, and any additional income and expenses, such as interest revenue.

Income statements also show a record of the business’s income before tax.

In many cases, income statements will have a record of COGS (cost of goods sold), which allows business owners to see how much money it costs to produce their goods, prior to turning a profit on the sale itself.

Therefore, Gross Profit = Revenue – COGS.

To further understand this, if the margins between the COGS and the gross profit are a close match, this is a key indication that the business owner is not making much profit off of each individual sale.

From the example of the income statement shown above, the following can be determined:

- The business earned $5 million in revenue, but it cost $2.5 million to produce the products.

- It costs the company a total of $500,000 to run the business (operating costs).

- The company allocates an additional $150,000 to cover unexpected costs unrelated to operating costs, including interest revenue, interest expense, and other extraordinary items.

- After taxes, the company makes $422,500; representing a 35% deduction of its original net income of $650,000.

How are balance sheets and income statements different?

While balance sheets provide a breakdown of assets, liabilities, and equity, income statements allow small business owners to better take stock of inventory and spending patterns to plan ahead, allowing them to make more informed business decisions for the next accounting period.

There are many similarities between balance statements and income statements.

It is important to remember that while income statements report the business’s revenues and expenses (profit and loss), balance statements keep a record of the company’s assets, equity, and liabilities.

As far as financial statements are concerned, most small business owners can make due using balance sheets and income statements.

However, in some cases, a third kind of financial statement, known as the cash flow statement, can further help business owners determine where their funds end up.

Cash flow statements

Cash flow statements are not always used as a standard business practice.

Generally, they’re used by companies that rely on the accrual accounting method, which tracks expenses only after a transaction takes place, as opposed to when a payment is made or received.

Cash flow statements indicate revenue that a company has secured, but may have not yet received. Therefore, that particular transaction will still appear as a source of revenue on the income statement.

Think of cash flow statements as a friendly record of an I.O.U. from the supplier.

Much like the balance sheet and the income statement, the cash flow statement is divided into various parts and usually provides data for operating activities, investing activities, and financial activities.

Operating Activities

The cash flow from operations indicates how much a business earns on a daily basis. Cash flow statements also keep track of how much the company is pending, and where those funds are being allocated.

Investment Activities

The cash flow from investments outlines how much profit a business has earned based on its investment purchases on behalf of the company.

Financing Activities

Cash flow from financing is similar to a balance statement’s liabilities. It’s an indication of the sources of cash from any investors as well as banks.

This section also refers to any money that a business owner has invested in the business. It also includes any outstanding debts, such as loans.

One of the easiest ways to increase a business’s cash flow is to process the accounts receivable at a faster rate.

Rather than providing a grace period of 90 days on an invoice, for example, a small business owner could demand that all outstanding invoices be paid in 30 days of issuance.

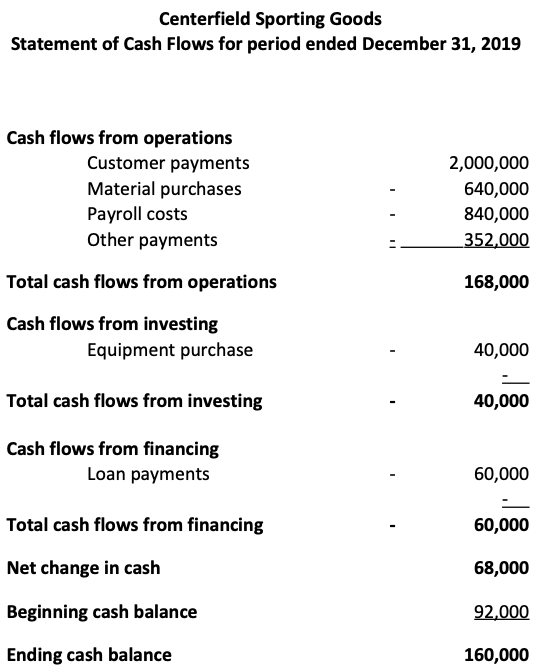

Below is an example of a cash flow statement:

In the above example, the following can be determined from the cash flow statement:

- The company’s total cash flow from operations equals $168,000. This reflects a combined sum of customer statements, material purposes, payroll costs, and other purchases.

- The company invested $40,000 from equipment costs into the business.

- The company took out a $60,000 loan.

- All investments and financing costs aside; the company made $68,000.

Using financial statements to grow your small business

Financial statements, once fully understood, can actually be incredibly beneficial to every small business owner. They may not always be the most fun part of the business day, but, over time, can be an integral part of any company’s underlying success.

Different kinds of financial statements can provide a number of further earning potentials, based on their ability to help business owners navigate their spending patterns and keep track of cost and profit margins. Small business owners can benefit from keeping a record of their financial statements for a number of reasons.

For starters, these documents are a business owner’s proof of the company’s overall performance and activity. This is attractive to any potential investors who may consider partnering or purchasing stocks or shares but are looking for an idea of how the business is performing.

Financial statements better track business spending

Financial statements also allow financial analysts to track better and predict the future revenue streams of the company. Without financial statements, a business owner cannot easily prove any incoming revenue or justify any expenses, or offer any direct insight into the company’s performance.

Using a cash flow statement, for example, is one way to help any small business grow, as this type of financial statement is an annual track record of all cash that was collected and paid out. This allows small business owners to predict upcoming expenses and better understand where there may be a surplus or a shortage of cash on hand. In turn, this helps small business owners make more informed spending decisions and allows them to prioritize certain parts of the company where finances are concerned.

Investing in assets is another way to expand business operations. By keeping a record of income statements, small business owners are able to forecast when expenses will pop up and plan accordingly to offset the costs.

Without a track record of those income statements, business owners are simply not in a position to accurately cast financial predictions and forecasts. Having a record of financial statements also helps small business owners secure a loan, a decision that many entrepreneurs opt for when just starting out.

Much like leasing a new car or purchasing a home, small business owners seeking loans are always required to show proof of income. This includes spending habits, profit and loss, and the overall financial position of the company. Without a record of financial statements, banks are reluctant to hand out additional funding, which in turn, could make it harder for small business owners to secure a bank loan.

How financial statements make tax season easier

Most small business owners prefer to focus on the day-to-day operations of the company. For that reason, administrative and financial tasks, like creating balance sheets and financial statements tend to take a back seat. However, keeping financial records also comes in handy for small business owners during tax season.

Unlike regular employees, entrepreneurs and small business owners do not always have the luxury of receiving a neat and tidy T4 and T5 slip that provides a one-page summary of annual income. Tax season can be downright exhausting for small business owners, as they are solely responsible for tracking down every single invoice, and they usually have multiple suppliers to track down.

Keeping a steady record of financial statements, including the balance sheets, income statements, and cash flow statements, better equips small business owners for tax season, as they will be able to generate an accurate report in a timely fashion. Most small business owners also incur business expenses which are permitted to be written off during tax season. Jotting those expenses down ahead of time means less time is spent pouring over old receipts, and more time preparing for future success.

Why financial statements matter

Financial statements don’t have to be complicated.

They are composed of three different types (balance sheets, income statements, and cash flow statements). Financial statements serve as a written record of a business’s day-to-day operations; balance sheets breakdown a company’s assets, liabilities, and equity.

And income statements serve to analyze a company’s revenue and expenses (profit and loss) over a certain period of time.

Lastly, cash flow statements provide financial analysts and potential investors with a more accurate idea of how financially equipped a business is to both fund its existing operations and pay back any outstanding debts.

Strong accounting is crucial for every small business. By keeping an organized record of financial records, all small business owners can easily build their own financial statements, thus making it easier to determine profit, loss, and future financial trends.

This article offers general information only, is current as of the date of publication, and is not intended as legal, financial or other professional advice. A professional advisor should be consulted regarding your specific situation. While the information presented is believed to be factual and current, its accuracy is not guaranteed and it should not be regarded as a complete analysis of the subjects discussed. All expressions of opinion reflect the judgment of the author(s) as of the date of publication and are subject to change. No endorsement of any third parties or their advice, opinions, information, products or services is expressly given or implied by RBC Ventures Inc. or its affiliates.